Volatility made a comeback this week. All it needed to destabilize financial markets was another Covid variant and commentary from U.S. policy makers signaling an eagerness to taper down the bond-buying stimulus program and move to hike rates. The release of disappointing U.S. jobs data also added to the woes. Meanwhile, several countries are tightening restrictions on travel and leisure and the risk is that this development will boost inflation as world trade is once again disrupted. Euro zone consumer price inflation hit a record high and “transitory inflation” has been replaced by “persistent inflationary pressures”.

Hover Over A Country To See Key Data And Over A Black Round Marker To See The Indices. Click On The Plus Or Minus Sign To Zoom In Or Zoom Out. Select The Home Button To Get The Map Back To Its Original Size

AMERICAS

CANADA

The Canadian market’s main index shed 2.32% in the week.

Healthcare and information technology shares dropped sharply on Friday. Real estate, industrials and consumer discretionary stocks were the other major losers.The Canadian economy added a net 153,700 jobs last month, far above market expectations of about 35,000 jobs. Canadian workforce has now seen six successive months of expansion. The unemployment rate in Canada fell to 6.0% in November from 6.7% in September, below market expectations of 6.6% and within 0.3 percentage points from the jobless rate recorded in February of 2020. It was the sixth straight month of decline.

U.S.

U.S. stocks fell broadly in a volatile week of trading.

The major averages went on a rollercoaster road as fears related to tightening U.S. monetary policy weighed. Traders also reacted to a closely watched report from the Labor Department showing much weaker than expected U.S. job growth in the month of November. The report said non-farm payroll employment rose by 210,000 jobs last month well below the Bloomberg consensus estimate of a 550,000 rise, while October’s figure was upwardly-adjusted to an increase of 546,000.While job growth in November registered its smallest gain this year, the unemployment rate fell to 4.2% from October’s 4.6% rate, and the labor force participation rate rose to the highest level since March 2020.

LATAM

In Chile stocks, as measured by the S&P IPSA Index, returned -4.58%. Chile’s Codelco, the world’s largest copper mine, foresees copper price around US$3.80 – US$3.90 per pound next year.

In Brazil, the Bovespa jumped 3%. Brazil’s third-quarter GDP disappointed (-0.4%), meaning Brazil is in technical recession as extreme weather conditions, high interest rates and inflation cut short its recovery. The country’s industrial production shrank 0.6% in October, compared to September, according to the Monthly Industrial Survey – Physical Production (PIM-PF),by the Brazilian Institute of Geography and Statistics (IBGE). In currencies, rising inflation and interest rates mean extremely volatility in 2022 for Latin American currencies, experts say.

ASIA/PACIFIC

JAPAN

Equities registered losses for the week as the country closed its borders to foreign nationals.

On the bright side, the services sector continued to expand in November, and at the fastest pace in more than two years on a jump in new business, the latest survey from Jibun Bank showed. Furthermore, industrial output rose 1.1% in October from the previous month, the first increase in four months, with the motor vehicle industry the largest contributor to the increase. The unemployment rate fell to 2.7% in October, better than the 2.8% consensus forecast and registering at the lowest level since March 2021, amid labor market tightness. Retail sales in increased 1.1% m-o-m in October, beating market estimates of a 1.6% fall likely reflectinga recovery in demand.

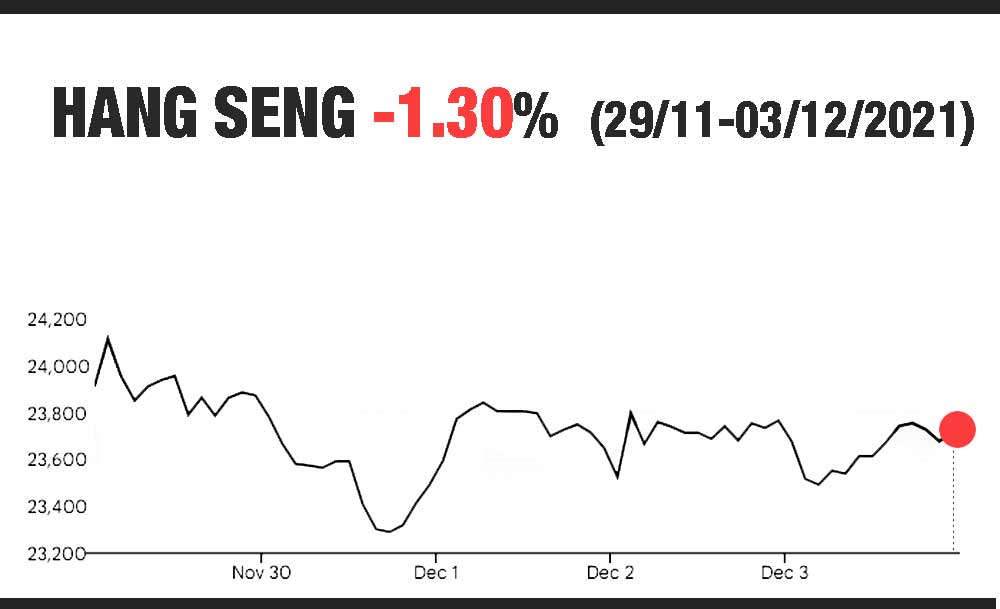

CHINA

Equities recorded a weekly gain despite a resurgence of U.S.-China tensions.

Chinese tech stocks in Hong Kong plunged after Chinese ride-hailing app Didi announced Friday that it

would delist its U.S.-listed shares from the New York Stock Exchange — less than six months after it made its debut stateside. The company also said in the statement that it will pursue a listing in Hong Kong.News of Didi’s delisting came amid pressure from authorities in Beijing and increased scrutiny from the U.S. Securities and Exchange Commission.

In economic news, China’s factory activity China’s official manufacturing PMI in November unexpectedly rose to 50.1 vs. 49.6 expected. However, the private Caixin/Markit Manufacturing PMI, fell to 49.9 in November from 50.6 in October. On the property front, developer Kaisa Group Holdings Ltd. failed to receive bondholder approval for a $400 million debt swap designed to avert default. That could spur contagion.

AUSTRALIA

The ASX200 was down 0.52% for the week and up 9.93% since the beginning of this year.

Investors digested a host of reports. Australia’s GDP expanded 3.9% on year in the third quarter, beating forecasts for an increase of 3.0% following the 9.6% jump in the previous 3 months. The services sector continued to expand last month, and at a faster pace, the latest survey from Markit Economics revealed on Friday with a services PMI score of 55.7. That’s up from 51.8 in October. The country had a seasonally adjusted merchandise trade surplus of A$11.22 billion in October while retail sales climbed 4.9%.

EUROPE

EUROZONE

European equities posted mixed results.

The week was highlighted by new lockdowns and further evidence of inflationary pressures. Eurozone’s consumer price inflation accelerated to 4.9% year-on-year in November, from 4.1% in the previous month and above market expectations of 4.5%, a preliminary estimate by Eurostat showed. It would be the highest rate of inflation since July 1991, and well above the European Central Bank’s target of 2.0%, as energy cost rose sharply (27.4%).

Inflation in Europe’s largest economies also accelerated to multi-year highs, with sharp rates being recorded in Germany (6.0%, the highest level since 1992), Spain (5.6%), Italy (4.0%) and France (3.4%).

Consumer morale decreased for a second consecutive month in November, according to a survey by the European Commission. Households are less upbeat about the general economic situation and their intentions to make major purchases as surging inflation has started to bite on people’s income.

CEE/SEE

Poland’s stocks posted gains.

Polish data this week showed annual inflation rate likely jumped to 7.7% last month, the highest rate since December of 2000, adding to expectations of further rate hikes and boosting the zloty. Most central European currencies are set to strengthen in the next year, guided by economic recovery and interest rate hikes, a Reuters poll showed.

In Romania, equities ended the holiday-shortened week also with gains. The Bucharest Stock Exchange was closed on Tuesday (Nov. 30) and Wednesday (Dec. 1) in observance of St. Andrew’s and National Day respectively.

In currency news, Romania’s forex reserves fell by EUR560 million in November versus October, to EUR39.2 billion, central bank data showed. Three out of ten managers in Romania anticipate exchange rate of 5.05- 5.10 lei/euro in 2022, according to data included in the third edition of the annual Moneycorp Barometer.

REST OF EUROPE

Russia’s equities as measured by the MOEX index jumped 2.68% this week.

Meanwhile, Russia Trading System (RTS) saw the index touching 1,900 in November – a level it hasn’t visited for nearly a decade and is now returning around 20% YTD. In economic news, the country’s manufacturing activity continued to grow in November with the headline seasonally adjusted IHS Markit Russia Manufacturing PMI posting 51.7.

In the UK, the main London index climbed 1.11%. Bank of England Monetary Policy Committee member Michael Saunders, who voted for an interest rate hike in November, indicated that he could vote against a rate hike this month. The Financial Conduct Authority (FCA) confirmed a list of changes to its listing rules, in an effort to bolster incentives for innovative founder-led companies to list on UK markets sooner.

In Switzerland, the SMI was off 0.19% this week as the mood turned cautious.

MIDDLE EAST

(Note: Trading 28/11-02/12/2021 except Turkey)

In Israel, trading in the Tel Aviv Stock Exchange (TASE) over the week was marked by decreases in prices in the leading share indices, similar to the trend in stock exchanges worldwide. The TA-35 index decreased 1.41% over the week, bringing year-to-date cumulative gains to 24.7%.

TASE has posted for public comments the rules for the listing of Special Purpose Acquisition Companies (SPAC).

In a new report, the Organisation for Economic Co-operation and Development (OECD) projected solid future GDP growth for Israel. The state “is projected to grow robustly by 6.3 percent in 2021, 4.9 percent in 2022 and 4 percent in 2023.”

In Turkey the BIST 100 Index returned 7.54%.

The Turkish equity market performed well in local currency terms The lira’s weakness, however, continued, as President Recep Tayyip Erdogan replaced the country’s finance minister after weeks of economic turmoil in which inflation soared. The Turkish Central Bank intervened in the currency markets on Wednesday to prop up the nosediving lira, which has lost more than 40 percent of its value against the US dollar this year, making it the worst-performing of all emerging market currencies.

AFRICA

In South Africa, stocks as measured by the JSE Top 40 index returned 3.04%.

Inflationary pressures are mounting and The Department of Mineral Resources and Energy on Wednesday announced the ninth monthly jump in the regulated gasoline price this year.

The series of fuel price increases took the total increase for 2021 to 40%. “We think the risks to inflation over the next six months seem firmly skewed to the upside,” Bloomberg quoted Jeff Schultz, a senior economist at BNP Paribas South Africa, as saying. South Africa’s jobless rate stood at 34.9% for the third quarter – a record high.

In Nigeria, equities plunged 2.63% this week.

On Friday, Nigeria’s Stock Exchange market cap dipped by N41.78 billion as investors sustained profit-taking At the close of market, the stock exchange market value stood at N22.00 trillion. On the bright side, the blue-chip index has advanced 1,897.19 base points since the start of the year.

Content Disclaimer:

This page has been prepared for informational purposes only. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.

For any comments, suggestions or corrections email: kbalkoudi@worldmarketsdaily.com

Kyriaki Balkoudi is a markets editor for World Markets Daily. She has a bachelor’s degree in Balkans Studies from Aristotle University of Thessaloniki, Greece and a master’s degree in International Politics from City University London, UK.

References:

“Global Markets Weekly Update”. T. Rowe Price. Dec. 3, 2021

“Weekly market wrap”. Edward Jones. Dec. 3, 2021

“Weekly Market Recap”. John Hancock Investments. Dec. 3, 2021

“Schwab Market Update”. Charles Schwab. Dec. 3, 2021

“Market Analysis”. Edmond de Rothschild. Dec .3, 2021

Read previous week’ s WM Review

Read all WM Weekly Reviews

Read about world stock exchanges CEOs, insights, events and more

Read weekly reviews about Bucharest Stock Exchange (BVB)