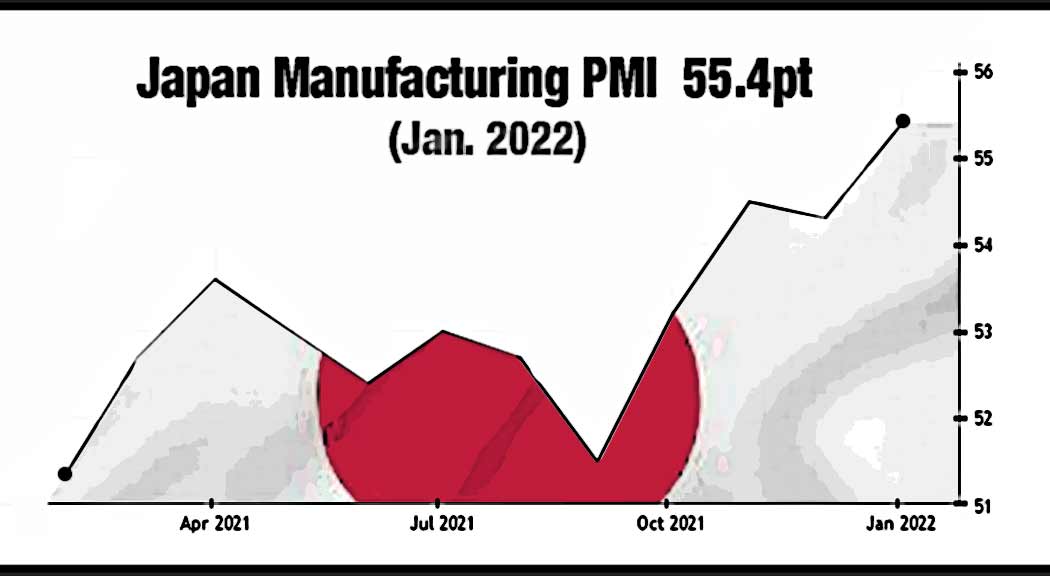

The manufacturing sector in Japan picked up steam in January, the latest survey from Jibun Bank showed on Tuesday (Feb. 1).

The au Jibun Bank Japan Manufacturing PMI was revised higher to 55.4 last month from a preliminary reading of 54.6. That’s up from a final 54.3 in December, and it moves further above the boom-or-bust line of 50 that separates expansion from contraction.

Latest data pointed to a sharp expansion in output despite pressure from a persistent chip shortage. Growth was recorded for the fourth consecutive month and was the strongest since February 2014.

Higher production levels were often associated with rising new orders with the latter rising at the fastest pace for nine months.

“Japanese manufacturers entered the new year in strong spirits as they reported a stronger improvement in the health of the sector. The latest Manufacturing PMI signalled that firms had begun to shake off the impacts of the pandemic and supply chain disruption to record the sharpest upturn in operating conditions in operating conditions in nearly eight years,” Usamah Bhatti economist at IHS Markit which compiles the survey said.

Respondents linked higher sales to improved client confidence in both local and foreign markets. As such, international demand for Japanese manufactured goods continued to expand at the start of the new year, with the rate of growth quickening from that seen in December, as companies cited stronger demand in key markets for sectors such as automotives and semiconductors.

However, the sharp surge in manufacturing activity further pressured global supply chains which remain disrupted due to uneven recovery from the Covid crisis around the world. Higher raw material prices drove up input price inflation with companies passing on some of these costs to consumers, driving up output prices at the fastest pace seen in over 13 years.

The Jibun Bank Japan Manufacturing PMI is compiled by IHS Markit from responses to monthly questionnaires sent to purchasing managers in a panel of around 400 manufacturers. The panel is stratified by detailed sector and company workforce size, based on contributions to GDP.